With the events of 2020 as our backdrop, we set out to capture how people are seeking happiness and wellbeing today, and how this is driving new behavior and expectations towards brands. Our approach combined a mix of methodologies to produce a unique view of the post-2020 consumer.

Our in-house Culture + Trends team, along with our leading-edge Illume Network and global Advisory Board, have identified 14 consumer trends based on the shifts in human drivers used to maximise happiness. Quantification amongst mainstream adult consumers in 16 markets globally shows the extent to which consumers identify with these trends and the impact on their buying behaviour.

The quant results showed us that four of the 14 trends were significantly more present among Generation Z (Zoomers) and Millennials aged 18 to 40, compared to the 40+ population. One overall conclusion is that the majority of these NextGen trends seem to be related to the mind, confirming the increasing importance of mental wellbeing for the younger generations that are missing out the most on social contacts and milestone celebrations due to the pandemic.

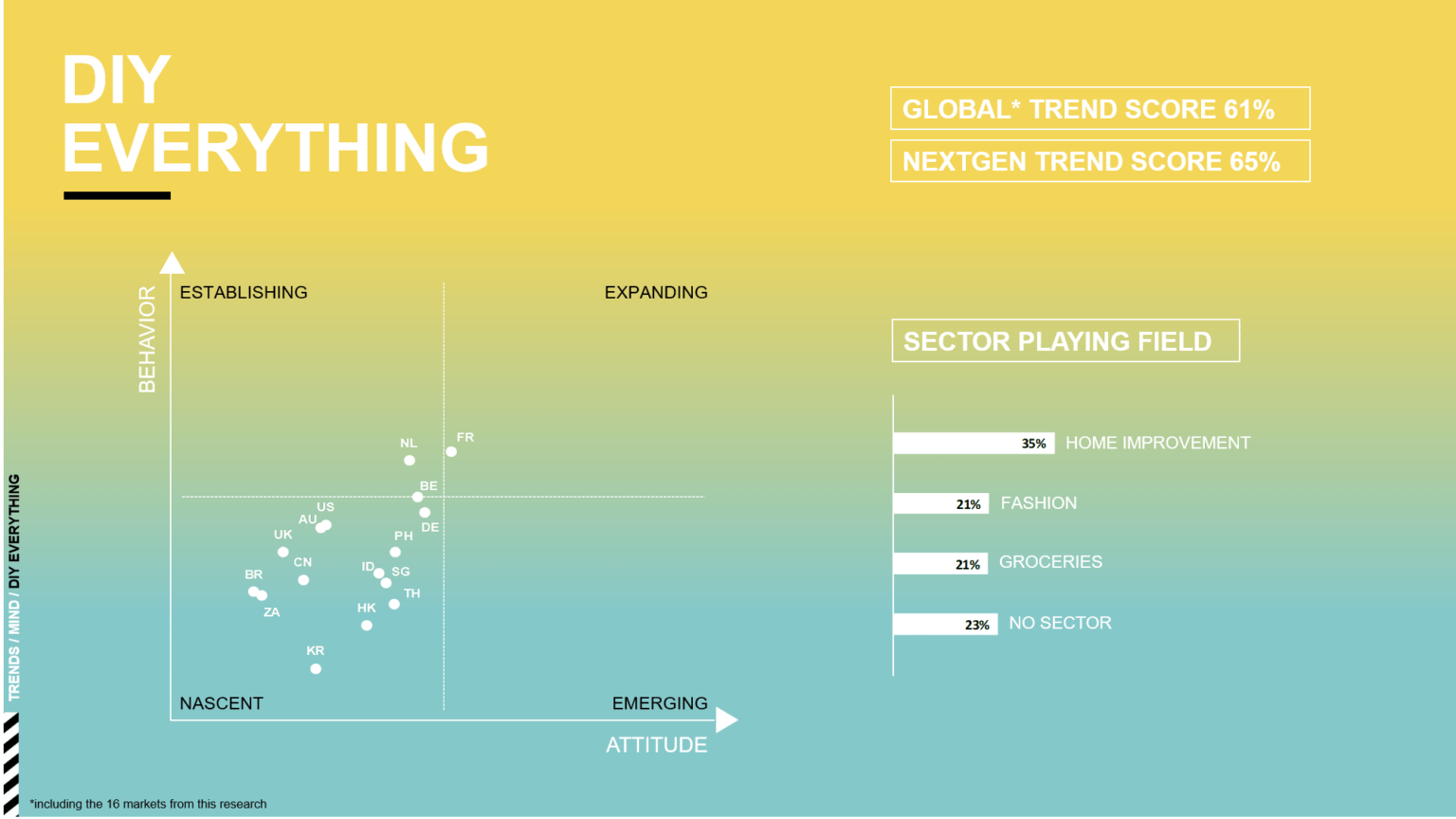

DIY Everything

‘DIY Everything’ is a trend that is driven by an increased need to express individuality alongside a strong shift towards more sustainable living. The pandemic has accelerated both of these needs, as consumers in general, and especially the younger ones, are re-evaluating their ‘ikigai’ (a Japanese concept that means ‘a reason for being’). DIY offers control overused ingredients or processing methods as well as the carbon footprint, while the active engagement in new skills gives a sense of purpose and achievement.

‘DIY Everything’ is a nascent trend amongst global markets, with a trend score of 61% for the general population compared to 65% for NextGen. Younger consumers are looking for daily activities that provide structure and distraction from the boredom of the pandemic restrictions. They are adopting new hobbies and crafts, from learning a new language to courses in cooking or coding. Brands across categories should create platforms and tools to collaborate with consumers on making hyper-personalized products and services. We’ve already seen a multitude of brands tapping into the ‘DIY Everything’ trend, not just in the home improvement sector, but also across fashion, as seen in Reebok’s first pitch concept and Raeburn’s collaboration with Depop.

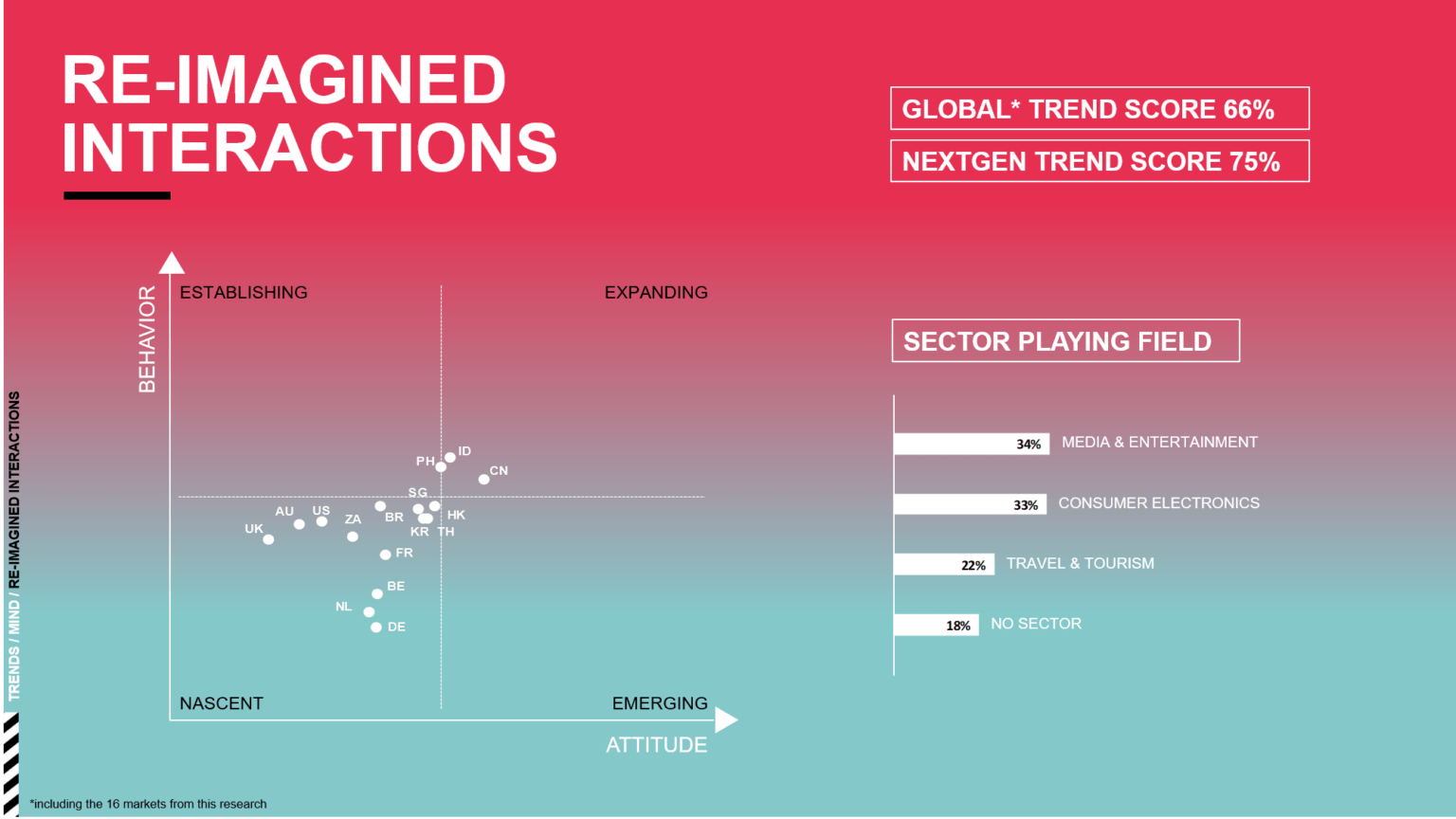

Re-imagined Interactions

‘Re-imagined Interactions’ is an expanding trend amongst NextGen consumers (trend score 75%) yet it is nascent with the general population (trend score 66%). In the past year, most of us have had to find new ways to organize our social interactions with friends, relatives, colleagues, and peers; but as consumers spend more time on screens than ever before, with a digital detox desirable for many, travel and mobility restrictions force us to re-imagine our interactions for now.

For many Gen Z consumers, the path to adulthood, including plans for education, has been disrupted by the pandemic. Many have been forced to live at home with their parents, whilst others have been renting off-campus shared housing, remote-learning together. In the US, A Place Beyond recently transformed sites normally used as American summer camps into learning communities, with a tailored schedule of guided outdoor activities, soft-skill workshops, and academic support. Meanwhile, John Hopkins University gave free Minecraft access to all enrolled students when they could not return to campus, and organized official school events inside the game, such as the annual Oktoberfest.

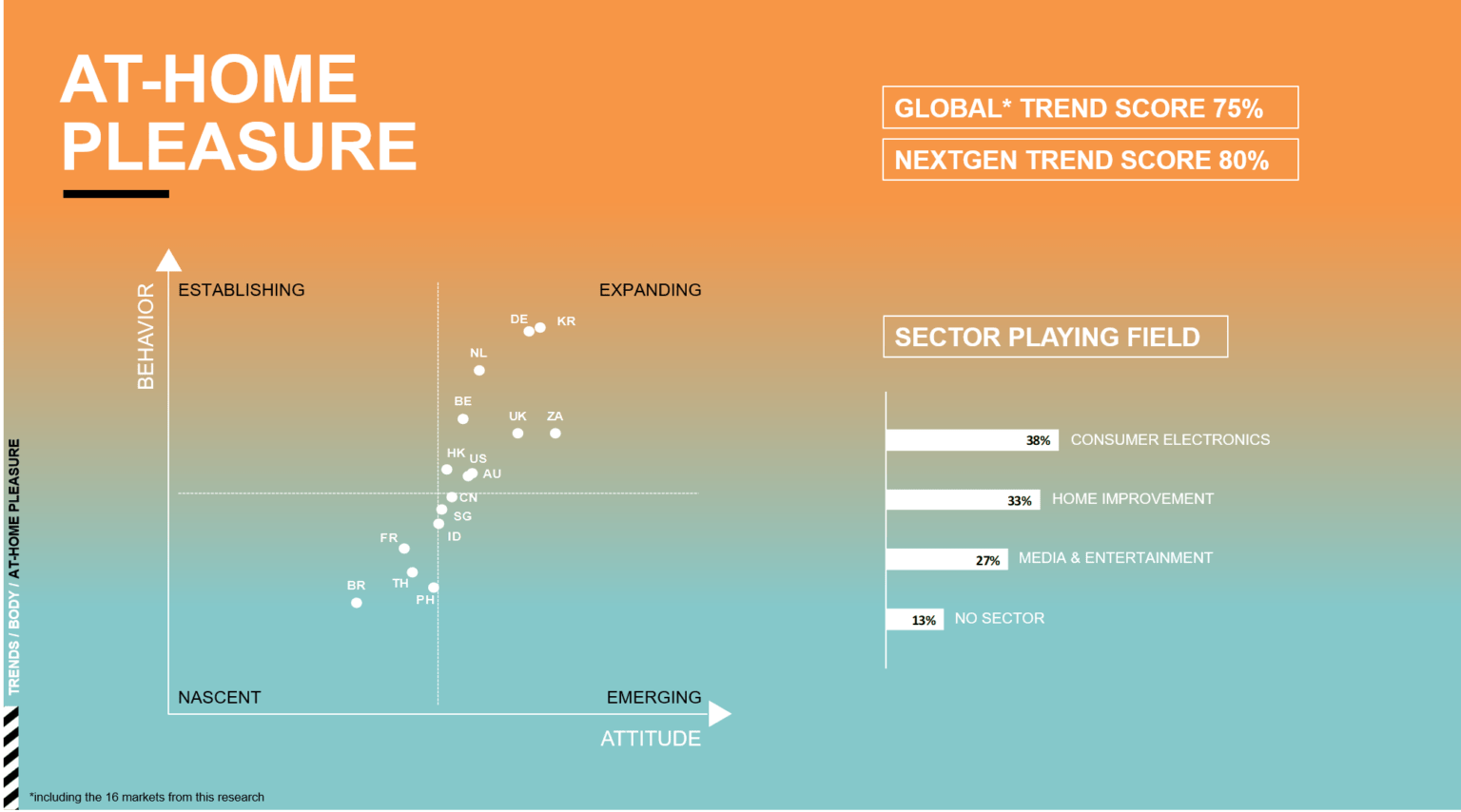

At-home Pleasure

Similarly related to spending more time at home, ‘At-home Pleasure’ describes the trend of people being eager to improve their home’s interior and exterior, adding new functions such as a fitness or home-spa due, to an unwillingness to compromise on luxurious and rewarding ‘me time’ whilst being confined to the home. This creates opportunities for brands that bring those types of me-moments into the home. Consumers are looking for new ways to experience highly pleasurable experiences in a familiar environment.

This trend is expanding globally, with a general-population score of 75% and an even higher NextGen score of 80%. Consumers are using money they would normally spend on holidays and going out, on staying in, with a focus on home improvement. Outside this sector, we see consumers globally looking for a companion at home, with more than 11 million households in the US having adopted a pet during the pandemic. This has led to a steep growth in related categories such as pet grooming and pet food, with ice cream brand Ben & Jerry’s launching Doggie Desserts and skincare brand Burt’s Bees branching into natural pet care products.

Wild & Weird

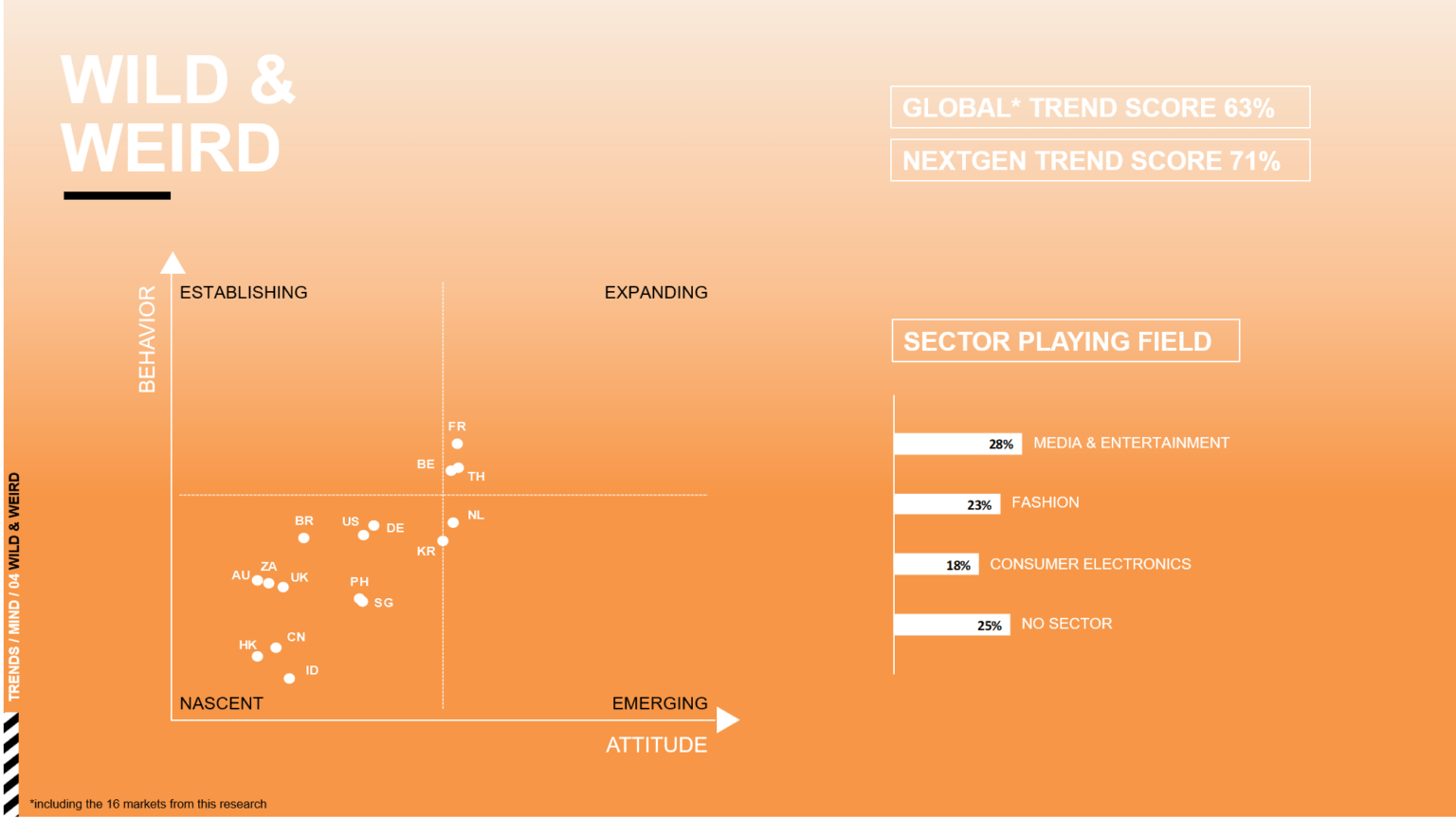

Last but not least, ‘Wild & Weird’ is a trend that is all about finding moments of spontaneity and silliness in a world of relentless negativity and stress. Brands can inject playfulness and fun into people’s lives, from digitally-driven satire or social media challenges to all things wonderfully weird. The ‘Wild & Weird’ trend has lower trend scores overall, with 63% amongst the general population, falling into the nascent quadrant, compared to 71% amongst NextGen.

The leading sector for this trend is media and entertainment, with social media platforms becoming the home of wild and weird content during the pandemic, from TikTok’s #nuntok trend to Instagram’s repetition accounts like @samepictureofatoaster and YouTube’s Sassy Justice channel. Just as disco music brought relief during the oil crisis in the ‘70s, we expect to see much more colorful, mood-lifting and nostalgic content released in the next months. Netflix’s hit show Bridgerton, set in the competitive world of the Regency era, uses a soundtrack of orchestral covers of pop hits by Billie Eilish, Taylor Swift and Ariana Grande. It was recently labeled the best new series ever, having been watched by over 82 million households in a 28-day period.

Of course, the global analysis presented in our 2021 Culture + Trends Report: Happiness Reset is just the tip of the iceberg, and we know that true value comes through the application of this unique methodology in real-world business challenges. Now is the time for brands to act. Which culture shifts and emerging trends are shaping your consumer, your category, and your brand?